Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The London stock market is not what it was. Listings are scarce. Successful listings are scarcer. Chest-beating pundits blame the depressed post-Brexit economy, red tape and yield-hungry fund managers. These factors have supposedly lumbered London with a large structural valuation discount.

Should UK private investors flee this scene of misery? Should they instead plug their savings into Vietnamese EV stocks or Bolivian silver mines?

Perhaps not. The structural discount thesis has a challenger in the form of James Arnold, a banker at UBS. Analysis by his strategic insights team suggests City declinism has been inspired by comparing British apples with American pears.

It is undeniable that the UK market broadly trades at a depressed price-to-earnings ratio. Before the 2016 Brexit referendum, it traded in line with the global average at about 15 times forward earnings. If you stripped the US out of the comparison, there was even a small premium.

Since 2016, the standing of the UK has progressively deteriorated. The discount hit a record level of 40 per cent against world stocks at the end of last year. The gap was 20 per cent against the world ex-US. The UK now trades on just 10 times forward earnings.

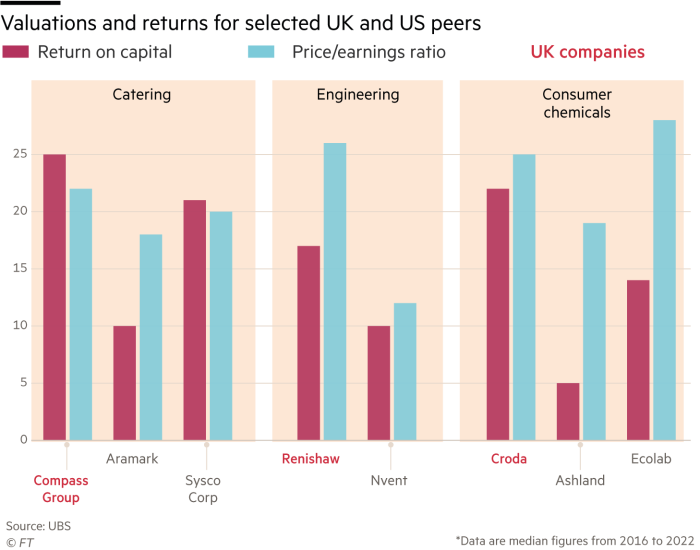

Arnold’s quibble is that these comparisons are not like-for-like. His team paired 60 big UK blue-chips with US peers they judged to be closest in type. Pairs included caterers Compass and Aramark, and engineers Renishaw and Nvent.

UBS found that the British stocks were either in line with US peers or higher in two-fifths of the cases. A big chunk of discount evaporated simply through the exclusion of a handful of US tech giants, such as Meta and Amazon. These have no real peers in the UK, or anywhere else.

The remaining difference points to a slim UK structural discount. This reflects higher US returns on capital, a function of lower taxes and a bigger domestic market.

A cynic might say you can support any thesis you like with handpicked data. Even so, UBS deserves credit for challenging accepted wisdom. It often turns out to be wrong.

One useful takeaway from the UBS analysis is that investing in indices is not the same as investing in the economy of the country. Indices are often quirky artefacts of history and stock exchange marketing campaigns. It is worth understanding their characteristics.

UK private investors can justify focusing on their local stock market on a couple of grounds, meanwhile. First, it removes the risk that the base currency of their investments may move out of line with liabilities denominated in sterling. Second, living in the UK may give them a better understanding of what domestically-oriented businesses are doing than foreign companies operating abroad.

Moreover, Arnold believes an inflection point is near. Only a slim sliver of UK defined benefit pension money is still invested in UK stocks. Defined contributions and other alternative retirement savings should now start mounting up. That should support broad market valuations, as well as the kind derived from like-for-like comparisons.

Milan, darling, Milan

Milan style beat The London Look on Tuesday. UniCredit and Barclays both exceeded profit expectations for the third quarter. The Italian bank, which is also active in Germany and eastern Europe, made the better impression.

UniCredit investors shrugged at confirmation of a €6.5bn capital return and higher revenue targets. But weak net interest margins in Barclays’ home market sent its shares down by as much as 8 per cent.

Rock-bottom valuations of banking stocks hint at economic weakness and imminent disaster. They are at levels only seen during past financial shocks. Investors see the rate-driven profits boom as yesterday’s news.

Returns on loans have soared most strikingly in southern Europe. Shares in UniCredit have been the best performing of any big European lender, up 70 per cent year to date. Investors foresee little in the way of further gains.

The benefits of rate rises are ebbing in the UK. Barclays’ UK net interest margins (NIM) — which measure the gap between a bank’s savings and loan rates — of 3.04 per cent undershot the figure of 3.12 per cent expected. Chief executive CS Venkatakrishnan cut full-year NIM guidance. Competition for deposits in the UK is growing. UK lenders have passed on higher rates to savers faster than continental peers.

“Low deposit beta”, as the pass-on rate is called, explains why UniCredit thinks it can squeeze out an extra €500mn of net interest income this year. Boss Andrea Orcel expects net profits of at least €7.25bn in 2023, and the same again in 2024. The expected return in dividends and buybacks is equal to an incredible 16 per cent annual yield.

UniCredit will avoid paying a tax on “windfall profits” imposed by the government of Giorgia Meloni. After news of the levy crashed bank shares, ministers gave lenders the option to reserve an amount equal to 2.5 times the notional tax charge. The figure for UniCredit stands at €1.1bn.

UniCredit shares have re-rated this year thanks to self-help and higher rates. It plans to compensate for peaking NIMs with steeper fees. Barclays will cut costs to protect its bottom line.

Only a diehard follower of depressed European bank stocks would spot much difference between the pair. UniCredit shares remain well below tangible book value at 0.7 times. Barclays stock is even less loved at 0.5 times. These metrics imply that the assets of both lenders are worth much less than their nominal value.

Price to earnings ratios of around five times have rarely been this low. These stocks look cheap — but they’re cheap for a reason.

The articles above are edited versions of pieces appearing in Lex, the FT’s flagship daily investment column.

Lex is the FT’s concise daily investment column. Expert writers in four global financial centres provide informed, timely opinions on capital trends and big businesses. Click to explore

Checkout latest world news below links :

World News || Latest News || U.S. News

The post Comparisons are odious for London’s stock market appeared first on WorldNewsEra.