Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

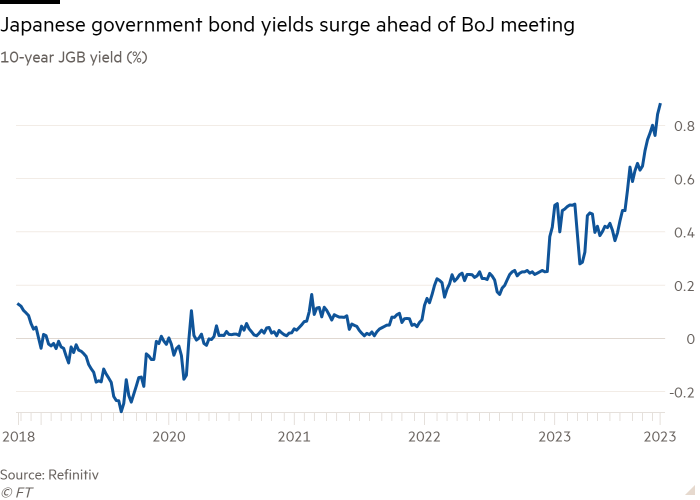

Expectations are rising that Japan’s central bank will relax its grip on the bond market this week as the yen tests a 33-year low and government bond yields touch the highest levels in a decade.

But investors’ bigger focus may be whether Bank of Japan governor Kazuo Ueda will offer crucial signals on inflationary trends that could pave the way for Japan to end the world’s last negative interest rates.

The yield on the benchmark 10-year Japanese government bond hit 0.89 per cent last week, the highest since July 2013. As a result, the BoJ is widely anticipated to revise — for the third time in 12 months — its unconventional “yield curve control” policy of buying government bonds to hold yields below a fixed level.

“It feels like the market is anticipating a modification to yield curve control and is starting to price that already,” said Jim Leaviss, chief investment officer for public fixed income at M&G.

The BoJ last revised the band within which 10-year JGB yields are allowed to trade in July. UBS now expects the bank to widen the band further on Tuesday, to 1.5 per cent from 1 per cent, and expects the 10-year JGB target yield of zero to be raised to about 0.5 per cent.

Barclays expects the BoJ to scrap yield curve control entirely on Tuesday.

However Goldman Sachs, Nomura and Morgan Stanley MUFG say the central bank is likely to stick to its current monetary policy framework.

The BoJ has been the only major central bank not to raise interest rates over the past two years, keeping its policy rate at minus 0.1 per cent despite 18 months of above-target inflation.

But the growing gap between borrowing costs in Japan and the US and Europe, as 10-year US Treasury yields surged to their highest levels in 16 years, has put pressure on the BoJ to tighten policy as the yen weakens.

The yen weakened past ¥150 against the dollar last week, raising concerns about inflation as the cost of imported goods rises. The ¥150 level has previously prompted currency intervention by Japanese authorities.

Although the yen has stabilised, currency traders see that as temporary and predict more severe tests if the BoJ does nothing following its two-day meeting on Monday and Tuesday, or makes only a cosmetic tweak to yield curve control.

Forex analysts said the Japanese government might be resigned to the idea that ¥152-¥153 is a fair level against the dollar. The widening differential between Japanese and US interest rates means intervention is likely to be less effective than in 2022.

Mid-October comments by the IMF, which said it saw no factors to justify intervention, add to a belief in markets that the ¥150 level no longer represents a “line in the sand” for Japan, even as the weaker yen keeps inflation above the BoJ’s target rate of 2 per cent.

The central bank has argued that the main factor pushing up prices in Japan has been the rise in imported costs and that it needs to wait for more sustainable signs of wage growth, to ensure that the economy does not fall back into decades of deflation.

In a speech in September, Ueda noted that wage growth was starting to have an impact on prices. Economists are paying attention to whether Ueda will acknowledge a stronger correlation between wages and prices.

“Even if the BoJ did not make any move this time, it will not be surprising if it started to deliver hawkish messages to prepare the public for a future rate hike,” UBS economist Masamichi Adachi said.

Japan’s core inflation in September fell below 3 per cent for the first time in more than a year on the back of lower imported fuel prices. Stripping out energy and fresh food prices showed inflation also slowed to 4.2 per cent from the previous month’s 4.3 per cent.

Still, some economists warn that Japan’s above-target inflation could be stickier than the BoJ is forecasting. In October, the Japanese Trade Union Confederation said it was seeking bigger wage increases during next year’s negotiations. Prime Minister Fumio Kishida has also pledged to raise minimum wages from ¥1,000 an hour to ¥1,500 by the mid-2030s.

Investors around the world watch Japanese bond yields closely because Japanese institutions are some of the biggest owners of US and European debt. More attractive returns at home could trigger a wave of selling in other bond markets.

“We think scrapping the YCC could trigger Japanese investors, but the more important driver is likely to be when the BoJ terminates the negative interest rates and starts raising short-term policy rates,” said Yusuke Miyairi, an economist at Nomura.

“The level of JGB yields is still not attractive enough for them to repatriate their capital from overseas into Japan,” he added.

Checkout latest world news below links :

World News || Latest News || U.S. News

The post Bank of Japan under pressure from weak yen and soaring yields appeared first on WorldNewsEra.