Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Friday was another glum day for the stock markets, ending a glum week and, indeed, a glum couple of months. Neither a strong GDP report, nor a few days’ pause in the upward march of interest rates, nor solid quarterly numbers from Amazon were enough to lift the mood. We provide our theory of what is going along below, but we are keen to hear yours: robert.armstrong and ethan.wu.

Why isn’t the market happier?

“Why is there something rather than nothing?” Philosophers call this the existential question. When I was studying the subject at Columbia some years ago, the legendary professor Sidney Morgenbesser, who had once trained for the Rabbinate, liked to offer what he called the Jewish answer to the existential question: “Even if there was nothing, you’d still be complaining!”

One might direct a similar comment towards the US stock market. The economy is booming, corporate earnings are strong, and yet the market is 10 per cent off of its summer highs and the momentum is steadily downward. The relationship between the economy and markets is never direct; there are many factors other than growth that influence equity prices. Still, the contrast is striking at the moment, and it is worth considering the reasons for it.

High valuations play a role here, but not in a simple way. Look at the chart below, showing forward price/earnings ratios for the S&P 500 over the past two decades. Valuations now look like they are at the high end of the recent average, but not terribly high for an economic expansion (although it bears mentioning that the valuations of the stocks that have led the market, the big techs, are quite demanding now, as we detailed last week):

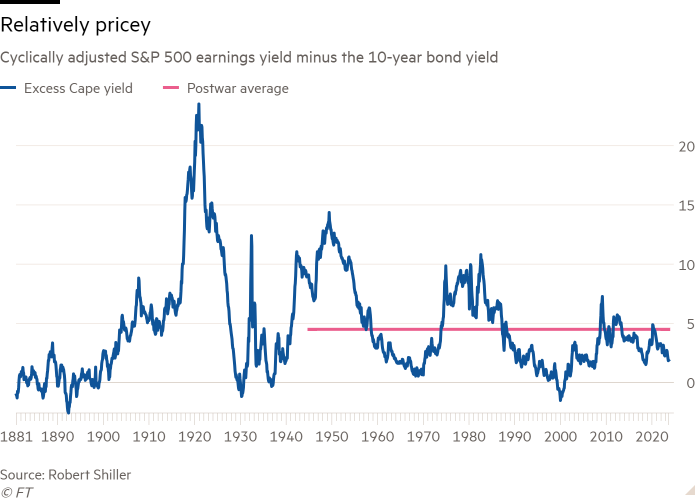

Valuations look like more of an issue when you add context, though, as Yale economist Robert Shiller’s metrics do. If you look at the cyclically adjusted earnings yield of the S&P 500 in excess of the 10-year bond yield (what Shiller calls the “excess Cape yield”), we are not at the horrific peaks of valuation reached in the dotcom bubble, but we are certainly paying a great deal for our corporate earnings, compared to the risk-free cash yield available in the Treasury market.

The valuation background helps explain why companies that miss earnings expectations are being punished with unusual harshness, as the FT reported last week. Current prices are not consistent with sub-par performance. The valuation picture looks even harsher for stocks when compared to corporate credit. Spreads remain tight, but absolute yields in high-yield bonds are in the high-single to low-double-digit range, while defaults remain muted and company quality has improved. Multi-asset investors have options.

It is, however, an Unhedged axiom that valuations are never a primary explanation for stock markets’ movement. They are a background against which other, more powerful explanatory factors operate.

One large but amorphous factor that is related to valuation and rates is uncertainty about change in financial and economic regimes. The period from the global financial crisis to the pandemic looks like a distinct period of moderate growth, low inflation and near-zero rates. If that era is over rather than on hiatus, then it is hard to say what appropriate asset valuations will be in the era that comes next. Historical comparisons like the one presented in the Shiller chart above may not be that much help.

Another possibility is that the market is signalling that the US economy’s purple patch might not be sustainable. Certainly, it will be a historical anomaly if the Fed raises interest rates by over 5 percentage points in record time and the economy responds with a sustained acceleration. Inflation that remains above target and an economy running hot allows the ghost of Fed mistakes past to rattle its chains ominously: the risk is the central bank pushes rates several notches higher at the precise moment that the first round of increases finally takes effect.

One especially fragile-seeming bit is the personal savings rate, which has fallen below pre-pandemic levels (see chart below). Without wading into a nebulous discussion of “excess savings”, the worry here is that the below-normal savings rate signals a consumer that is spending more aggressively than can be sustained. Last week’s bumper GDP report contained similar whispers of a future slowdown. So far this year, nominal consumer spending has grown about 1 percentage point faster than nominal personal incomes, suggesting that people may be spending out of savings. Don Rissmiller, economist at Strategas, notes: “Any significant cracks in the labour market could hit the consumer quickly with confidence already under some downward pressure.”

Stocks are also probably reacting to an increase in rate volatility. The 10-year yield has risen roughly two standard deviations, or about 50bp, in October, a move that historically coincides with the S&P 500 falling 4 per cent, according to David Kostin of Goldman Sachs. Any creeping up in inflation, far from unthinkable in a strong growth economy, could put another string of Fed rate increases on the table and send yields soaring even higher. Even an indeterminate growth/inflation picture could generate an erratic bond market and keep rate vol high.

Finally, it would be wrong to write off the possibility that after the increase in rates we have seen, something simply breaks. We had a taste of this in March when terrible rate risk management doomed Silicon Valley Bank and First Republic. While the rest of the banking system seems pretty stable to Unhedged, and many companies termed out their debt when rates were near zero, one cannot predict where and when the next institutional vulnerability is going to appear, and this risk surely rises as long yields do. The economy has proven resilient. Will every large hedge fund/private credit vehicle/real estate financing structure?

One good read

Great news about American wealth.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Checkout latest world news below links :

World News || Latest News || U.S. News

The post The unappeasable market appeared first on WorldNewsEra.