Meghnaghat, near the Bangladeshi capital Dhaka, was once a rural backwater of fishing hamlets and paddy fields. Today, it is dominated by the red-and-white smokestacks of gas-fired power stations.

Few places illustrate the speed of the country’s energy transformation better. Several plants are already active and three more are soon to open at the site, including a 590 megawatt project by Bangladesh’s largest private power producer, the Summit Group. At least one more facility is planned.

But there’s a catch: it is not clear where the gas to power Meghnaghat’s turbines is going to come from, or whether there is sufficient demand for the electricity that they, and other facilities throughout the country, can generate.

Bangladesh is one of a growing number of developing countries in Asia and beyond to have bet heavily on natural gas as a “transition fuel” — a reliable, affordable and cleaner alternative to coal or oil that helps reduce carbon emissions while they develop more renewable energy capacity.

The International Energy Agency expects that with gas demand peaking in mature European and North American markets, countries such as Bangladesh, the Philippines and Thailand will henceforth drive much of the growth in gas consumption. Global Energy Monitor, a pro-renewables non-profit organisation, estimates that nations in south and south-east Asia plan to increase their gas-fired power capacity by more than 50 per cent.

But a surge in the price of liquefied natural gas (LNG) has put a substantial bump in the road, with gas imported for power generation now in short supply and much more expensive than originally envisaged.

After heavy investment in new gas power stations Bangladesh — a low-lying country, extremely vulnerable to climate change — is now contending with dwindling domestic gas reserves and fuel shortages triggered by the steep increases in LNG costs. This combination of factors has led to blackouts and falling foreign reserves, both of which threaten an economy celebrated globally for its rapid growth and development gains.

“We’ve developed our power sector based on the perception that [LNG] is cleaner and more widely available,” says a Bangladeshi government official. “Now it’s a real challenge . . . The question is how we’ll manage if we’re not even feeding our existing plants.”

Critics of the oil and gas industry argue that, at a time when renewables are becoming more competitive and attractive, countries like Bangladesh risk tying their energy future to a fossil fuel that is not only not as clean as its proponents suggest, but whose supply can be erratic and its pricing volatile.

“Whereas coal is essentially limited to China and India, we’re still seeing gas plants being announced in every single region,” says Jenny Martos, a researcher at GEM.

“Relying on gas without having the fuel, and being subject to LNG prices, just doesn’t make sense.”

Lower-carbon growth

Natural gas emits about half the carbon of coal for the same amount of energy, leading supporters to argue that it could help developing countries wean themselves off dirtier fuels like coal and oil while allowing their rapid economic growth to continue. Importing gas in liquefied form meant even countries with limited or no gas reserves of their own could use it.

That certainly appealed in Bangladesh, whose indigenous gas supplies could not support a big expansion in power generation. When Prime Minister Sheikh Hasina came to power in 2009, the country was suffering from severe electricity shortages.

To rectify this, her government rolled out incentives for private power producers to construct new generation plants powered by fossil fuels, which in addition to generous capacity payments protect them from legal challenges and prosecution. To ensure quick supply, the country also pivoted to imported fuel, buying its first LNG cargo in 2018.

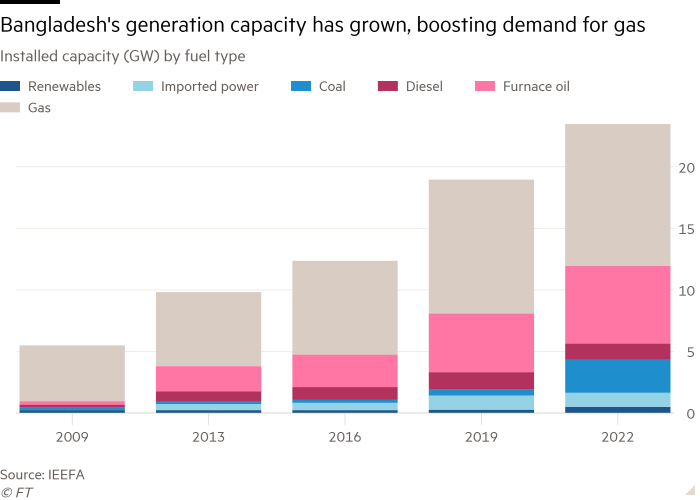

It worked. Electricity generation capacity soared from 5.5GW in 2009 to 23GW currently, according to the Institute for Energy Economics and Financial Analysis, a think-tank. As a result, Bangladesh’s entire population of 170mn now has access to electricity, compared with less than half in 2009.

Prioritising gas helped limit the country’s dependence on coal. While coal imports have also grown, it accounts for 12 per cent of the country’s generation capacity compared to 50 per cent for gas, according to the BloombergNEF, a commodity research service. In 2021, Sheikh Hasina cancelled plans to build 10 new coal-fired power plants.

Yet Bangladesh now faces problems of a different nature. Electricity demand did not keep up with the building frenzy, and total capacity now exceeds demand by as much as 50 per cent. The lack of investment in new domestic hydrocarbon exploration also means the country’s domestic gas reserves are running low.

That has left it at the mercy of global LNG prices. Unlike piped gas, LNG can be transported anywhere there are regasification facilities and cargoes tend to gravitate to the markets where prices are highest. Following Russia’s invasion of Ukraine, that market was Europe — prices rose so high that traders were willing to pay penalty clauses to Asian countries in return for diverting their cargoes westward.

Fuel shortages and a surging energy import bill pushed Bangladesh into one of its worst crises in years, with rolling blackouts and painful inflation. Foreign currency reserves have fallen about 20 per cent this year, according to rating agency Fitch, and the country has taken out a multibillion-dollar IMF loan to steady its economy.

A protest in Dhaka against power cuts. Bangladesh is now struggling as a result of dwindling domestic gas reserves and fuel shortages © Sony Ramany/NurPhoto/Reuters

“People’s lives had improved,” says Khadiza, a 60-year-old vegetable vendor in Dhaka. “But now we’re facing our toughest time. Before I could pay my rent and my children’s expenses, and save money. Now it’s all upside down.”

But Bangladesh’s challenge is not solely down to Russia’s energy war with Europe. The measures introduced over a decade ago to incentivise and fast-track the construction of power plants remain in place today — even though the country now has too many of them.

This means that even as Bangladesh struggles to afford fuel, more money goes towards capacity payments for projects that have in some cases been idle for more than a year. Bangladesh’s power sector subsidy burden jumped to Tk297bn (about $2.7bn) in 2022, the IEEFA said, 150 per cent higher than a year earlier.

The Summit Group has been a leading beneficiary of Bangladesh’s energy policies. Along with its upcoming plant in Meghnaghat, it is building several new LNG projects in addition to about 15 existing power plants. Of the Tk1tn ($9bn) of capacity payments by Sheikh Hasina’s government since it came to power, Summit has in recent years been the largest private beneficiary.

The Summit Gazipur power plant outside Dhaka in Bangladesh. The group is building several new LNG projects in addition to about 15 existing power plants © Orjan Ellingvag/Alamy

Muhammed Aziz Khan, Summit’s founder, argues that Bangladesh has no choice but to import more LNG if it wants to avoid burning coal. “The demand for energy is huge. It must be supplied,” he says. “It’s a moral, ethical, commercial requirement.”

But to critics, the continued gas buildout shows that the interests of these powerful and politically connected conglomerates have long since overtaken considerations about energy security. Khan’s brother is a parliamentarian and former minister from Sheikh Hasina’s ruling Awami League party. A representative for Summit did not respond to a request for comment on the matter.

The electricity these private plants produce, at about Tk10 per kilowatt hour, is also roughly double the cost of that generated by state-owned companies, according to IEEFA. The losers, analysts argue, are the Bangladeshi people.

“The major crisis that will be coming is energy security,” says Rashed al Mahmud Titumir, an economist at the University of Dhaka. He lists the challenges: “Overcapacity, high retail prices, fuel shortages and now a struggle to pay energy bills — while subsidising an oligarchic clientele.”

Dhaka’s dash for gas

The 10 years leading up to Russia’s invasion of Ukraine were what the IEA describes as the “golden decade of gas”, during which consumption increased 25 per cent globally thanks to buyers like China.

But the geopolitical turmoil has shaken confidence in LNG as a reliable fuel source, with gas prices also jolting higher on disruptions to Israeli gas production amid the conflict with Hamas.

Less than 3% of Bangladesh’s electricity comes from renewable sources despite a 2008 plan to get to 10% by 2020 © Anik Rahman/Bloomberg

A drop in prices from last year’s highs helped attract some renewed buying, with the Asian LNG benchmark price falling to $17.8 per million British thermal units (mmbtu) from an average of $34 per mmbtu last year. Bangladesh bought two LNG shipments on the spot market last month, Thailand boosted LNG imports to record levels this year and Vietnam bought its first-ever cargo.

But prices are still more than double their average of $6.7 per mmbtu between 2015 and 2020. Laurent Ruseckas, executive director for gas at S&P Global Commodities, says that while gas has an important role to play in helping developing nations in Asia meet their growing power demand, pricing remains a challenge.

It is further complicated by the fact that the credit risk of state-backed groups in emerging markets can be too high for producers and traders to offer them the kind of long-term supply deals that would minimise their exposure to price volatility.

New supply is likely to ease prices in the coming years, with a wave of new liquefaction capacity in Qatar, Mozambique and the US from 2025 onwards expected to allow more LNG cargoes to reach world markets.

What is less clear, however, is how much of that gas Europe will need and how much pressure that demand will put on prices. While the EU is targeting a steep cut in gas demand by 2030 to help eliminate its reliance on Russian fuel, Ditte Juul Jørgensen, the bloc’s top energy official, has also signalled that it will need US gas for decades to come.

Continued competition for supplies could still result in Asian countries that have invested in LNG infrastructure without affordable sources of the fuel losing out. The risk, analysts say, is that such countries may end up doubling down on coal, threatening the energy transition altogether.

Officials in Pakistan earlier this year told Reuters LNG was “no longer part of the long-term plan” and that the country would quadruple coal production instead.

“The economic case is not there with prices now,” says Anne-Sophie Corbeau, Global Research Scholar at Columbia University’s Center on Global Energy Policy. “For many of these countries, coal is cheaper, period. Gas is expensive.”

Missing out gas

Climate advocates argue that investment in renewables would make more sense than expanding gas-fired generation.

But Bangladesh has made negligible progress towards renewables so far. Less than 3 per cent of its electricity comes from renewable sources despite a 2008 plan to get to 10 per cent by 2020.

Sheikh Hasina has revived these efforts, saying that the country aims to get 40 per cent of its energy from renewable sources by 2041. But a draft version of the government’s upcoming integrated energy and power master plan, seen by the Financial Times, has changed the target to “clean” energy, which includes technologies such as carbon capture and storage, whose large-scale viability some have questioned.

Bangladesh now wants to find more domestic gas to relieve its dependence on LNG, with the draft master plan aiming to reactivate existing onshore fields and undertake “high-risk” projects to explore offshore.

Bangladesh now wants to find more domestic gas to relieve its dependence on LNG following Russia’s invasion of Ukraine

“The Ukraine-Russia war taught us that if we don’t have our own domestic gas then it’s difficult,” says the government official. Yet such projects, even if successful, will take years to develop — meaning that Bangladesh will depend on imported LNG for years to come.

“Some gas may be necessary,” says Sam Reynolds, an energy finance analyst at IEEFA. “But what we’re seeing right now is a total mismatch between what market fundamentals would dictate is necessary and what investor proposals and expectations are saying.”

Scaling up renewable projects is admittedly complicated. Analysts say land is in short supply in the densely populated country, while financial incentives continue to make fossil fuel projects more attractive to the private sector, resulting in a shortage of funding for renewables.

Some investment has begun to trickle in. Earlier this year, Saudi Arabia’s ACWA Power agreed to a joint venture to build a solar plant, while Summit also announced it would invest $3bn in projects to import clean electricity from renewable energy-rich neighbours like India and Nepal.

Ruseckas says the lack of local supply chains for the construction of renewable capacity means that it’s not “seen as plausible to skip gas” in countries like Bangladesh. “You still need gas in those markets. The challenge for those countries is how to fit it into the energy system and make prices work.”

But others argue that Bangladesh risks missing an opportunity. BloombergNEF suggests that the policy document has “ignored or underestimated” the country’s renewable potential, with solar electricity set to become cheaper than power from fossil fuels in the coming years.

Gas will result in a “never-ending transition”, says Hasan Mehedi, an activist with Bangladesh’s Coastal Livelihood and Environmental Action Network, arguing that the country should prioritise leapfrogging to solar.

“Why should you develop more and more [gas-fired] power plants when you don’t have enough gas?”

Checkout latest world news below links :

World News || Latest News || U.S. News

The post Will Bangladesh come to regret its dash for gas? appeared first on WorldNewsEra.